We use the same analytical rigour for analysing startups as we do for making sense of the financials of large companies. There’s a lot to be learnt from studying both – they are both businesses !

In the midst of Zomato’s IPO being heralded by many as a bellwether for the spate of upcoming tech IPOs, CarTrade, a profitable (yes you read that right) venture backed tech-enabled company filed its DRHP papers on May 15. Read on for our thoughts on the company and the broader used car space in this 2-part blog series:

Summary:

CarTrade is a multi-channel auto platform with coverage and presence across vehicle types and value-added services. It generates revenues from several business streams primarily comprising:

- commission and fees from auction for new/used vehicles including auto finance, insurance (Shriram Automall, CarTrade Exchange)

- online advertising solutions, lead generation, technology-based services (CarWale, CarTrade, BikeWale & AutoBiz)

- inspection and valuation services (Adroit Auto)

While a detailed breakup across service lines has not been provided, commission and related income from auction/sale of used cars has clearly emerged as the largest revenue driver for the company:

Broad financials for the company:

The Net Profit for FY-21(9m) has jumped from to Rs 851 Mn (2.7x jump from FY20). However, this is on account of the Parent Company recognizing a deferred tax asset in FY-21 due to a change in the management estimate with respect to utilization of certain portion of it brought forward losses and unabsorbed depreciation on account of goodwill not being considered as depreciable asset as per Finance Bill, 2021. This is likely to be a one-time adjustment and must be considered as such while assessing the company.

Further a significant portion of the company’s net profits are attributable to non-controlling interests (due to ~44% external shareholding in Shriram Automall), potential investors must thus consider the actual net profit attributable to shareholders of CarTrade while making their assessment

Multi-channel platform

The company has developed (CarTrade and CarTrade Exchange) and acquired several prominent brands (Carwale, Shriram Automall) to emerge as a comprehensive omni-channel automotive platform.

Its platforms, CarWale and BikeWale, rank number one on relative online search popularity, while Shriram Automall is a leading used vehicle auction platform based on number of vehicles listed for auction for the financial year 2020

CarTrade had ~ 8 lac vehicles listed on its platforms for auctions by Mar-21, while it had ~2.6 crore of Average Monthly Unique Visitors in FY21 demonstrating its ability to attract stakeholders on its digital platforms.

The company is led by Vinay Sanghi (former chief executive of Mahindra First Choice) and has raised ~USD 355 Mn over its lifetime from investors including Warburg Pincus, Temasek and JP Morgan to emerge as a digital automotive ecosystem which connects automobile customers, OEMs, dealers, banks, insurance companies and other stakeholders.

Industry:

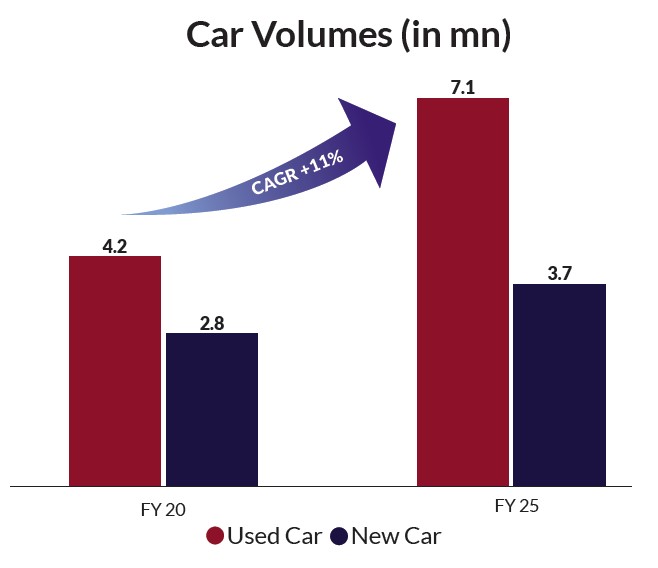

Between financial years 2016 to 2019, the Indian car market was one of the fastest-growing markets in the world, growing at a CAGR of 7%, although its growth was adversely affected in financial year 2020 due to factors such as the economic slowdown, Bharat Emission Stage -VI norms and change in insurance regulations. However, the used car market has picked up, growing bigger than the new cars market as it has continued to move towards getting formalized on the back of significant investments being poured into the sector fuelled by the increased need for personal mobility among price-conscious customers.

The gap in size of the pre-owned car market v/s the new-car market has increased from 0.5 Mn units in FY16 to ~1.4 Mn units in FY20. During this time frame, the used car industry has overall shown a CAGR of 6.21%, while the new-car industry had a negative CAGR of 0.09%.

The used-car industry in India has significant headroom to growth with low vehicle penetration in India (~30 per 1,000 people), while its Used/ New car ratio (~1.5x) is also amongst the lowest in the world.

For FY20 GMV of the new-car industry is 52% larger than the used-car industry. For FY25 it is estimated this gap will shrink to 12.5%.

Growth vectors for the used cars industry:

· Increased trust and transparency: The entire vehicle buying journey is undergoing a digital transformation – this has eased decision-making by stakeholders due to transparent data on pricing, condition, mileage etc. of used cars.

· Reduced ownership period: In FY11, the average replacement age of a car in India stood at 6 years, whereas as of FY20 this has dropped to 4.5 years. The faster churn lends itself to pre-owned cars for value driven Indians especially first time buyers.

· Government policy: A significant near-term factor is a favourable push through the PLI scheme, new scrappage policy, etc. This is important in the context of several regulations affecting key VC backed sectors – foreign investment in retail/ ecommerce, drones, RBI monitoring of fintech firms, etc.

· Digitization push by stakeholders: Dealers/ OEMs have also realized the value of online platforms and are poised to increase their digital spends substantially (The digital spend by OEMs is forecasted to grow at a CAGR of 23% for the next 5 years – ~$250mn in the year FY25 from the current <$100mn in FY20).

· Gap in Auto finance: There is a need to fill the gap in financing of vehicles, especially of used vehicles where interest rates are more attractive, while penetration for auto finance is still low at only ~19%. This This is estimated to increase to 30-35% by the year FY25, thereby increasing access to capital for a consumer to own a used car.

Key risks to growth of the industry

· Ride sharing/ Leasing trend: A growing share of younger people no longer purchase or lease their own cars, opting for ride-hailing services, ride-sharing services, car rental services and public transportation instead

· EV impact: India’s plans of moving towards a complete Electronic Vehicle led ecosystem may severely disrupt the used car industry

Future growth estimates:

As of FY20, the used-car market is 50% larger than the new-car market. In FY25 the used-car volume is estimated to be 90% larger than the size of the new car market in the country. The market is likely to be at 7.1 million units in FY25, representing $40 billion of GMV from $19bn as of FY20 with a CAGR of 17% and offering $7 billion of revenue-generating opportunities for value chain participants.

Formalization of the used car industry :

India’s used car market is witnessing a fundamental shift from unorganised to organised led by online car platforms.

The C2C (Customer to Customer) channel still holds a majority of 34% of all transactions in the used-car industry. However, this has dropped from the 40% share that it held in FY11. The share of transactions through the unorganised channel has significantly dropped from 30% in FY11 to 18% in FY20. This indicates that a considerable number of transactions have shifted from the C2C and unorganised channels to organised or semi-organized channels

TAM:

CarTrade has estimated its Total Addressable Market Size to be USD 14 Bn in its DRHP

Summary:

While CarTrade is well positioned to benefit from growth of the used car automotive sector and its formalization, on account of its prominent digital ecosystem complemented by its offline presence, the space is highly competitive with several well-funded players including the likes of Cars24, CarDekho and existing used car-business of automakers like Maruti True Value and Mahindra First.

We shall look to cover the competition landscape and our thoughts on valuation in the 2nd part of the blog. We would love to hear your feedback – write to Dhruv or Siddharth with your thoughts.

References: Malpani Ventures research, Company DRHP, IndianBlueBook (IBB) -2021

Note: The above must not be construed as investment advice.

Now having bought OLX India business the fortunes of the company should rise up again!